As COVID-19 induced unemployment swept the nation, Briana Bell was one of the fortunate ones who transitioned to remote working. The lack of commuting allowed her to cut back on daily expenses and focus on a bigger goal, owning a home.

Like other working-class millennials, the weight of a generational wealth gap and unprecedented college-related debt has tainted her credit and left her cash-strapped despite still being employed.

“Right now, [with the] student loans I have, trying to save is hard too when you don’t have [a family] gifting [you] a down payment,” said Bell, 30.

But hope is not lost. Bell, an insurance agent for Geico, wants to buy a home in the outskirts of Dallas, Texas, in the next five years.

Briana Bell, 30, is looking to purchase a home in the next five years.

Bell is part of a recent group of millennials (born 1981-1996) who are looking to make the long-term investment of buying a house as working remotely becomes the new normal. But qualifying for a mortgage and securing a down payment comes with a unique set of challenges for millennials, a generation marred by the Great Recession and the economic fallout of COVID-19.

“What’s interesting, pre-pandemic, we didn’t see a lot of interest in millennials wanting to own homes,” said Shannon McLay, founder of The Financial Gym, a consulting agency. “Work from home is becoming very big and they want to like where they work.”

In the past year, the housing market has been priming itself for a wave of new buyers. Interest rates on home loans have dropped to 2.9% from last year’s 3.64%.

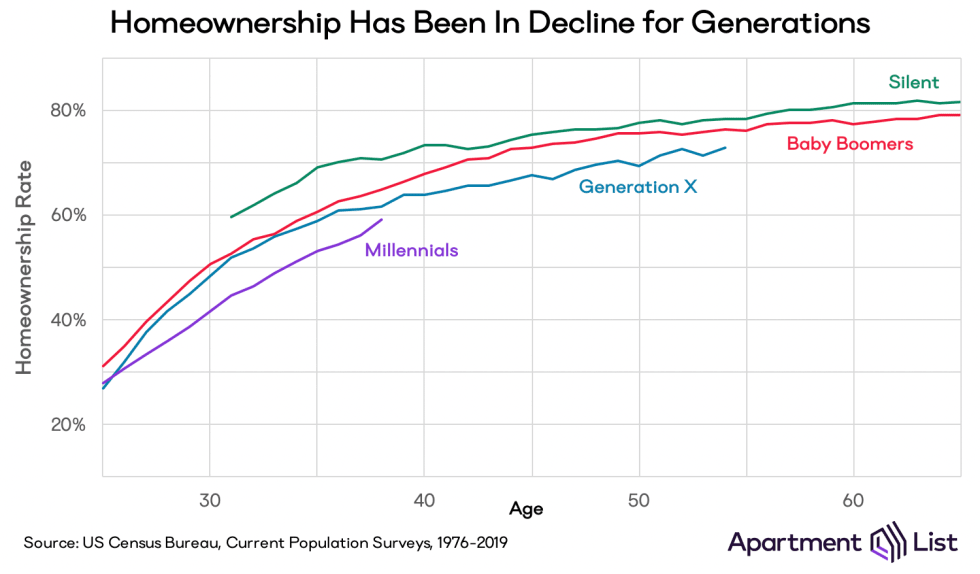

Owning property is one of the most common ways for Americans to grow wealth and earn equity. Yet home ownership for young adults like Bell – who are bogged down by mounting student loan debt and lower earning potential because of stagnant wages following the 2009 recession – is less common than it was for their parents and grandparents.

Still, financial advisers say purchasing a home in today’s market is feasible for adults aged 24-39, who face greater financial disadvantage than previous generations.

“Home ownership is definitely there,” McLay said. “It’s about putting a plan together for how you want to get there.”

Millennials looking to buy a house are aware they face more economic challenges than prior generations and are eager to repair their financial health, she added. The first step is knowing what you can afford and the kind of mortgage loan you qualify for.

About 28% of a homeowner’s income per month goes to housing costs. Before entering the market, create a budget breakdown to gauge your cash flow. After you know what you’re working with, find a suitable mortgage lender.

Interest rates on mortgages have fallen but the industry standard for a down payment is still around 20% of the home price. Since a lower income and credit score may pose a challenge for millennials reeling from student loan debt, experts say alternative mortgage lenders are a plausible solution.

Organizations like the Neighborhood Assistance Corporation of America, Federal Housing Administration and United States Department of Agriculture help people with income or credit barriers. These programs allow first-time home buyers to put anywhere from 3-5% on the down payment.

Location could also be a barrier to your first home. Financial advisers recommend exploring areas outside of big metropolitan cities like New York City and Los Angeles.

“When you live in an expensive city, it’s more challenging. When most of your paycheck is going toward rent, that’s going to make home ownership a further goal,” McLay said. “We’ve had clients rethink where they’re living … to get to that long-term goal.”

That’s what Analisa Cantú did. After leaving her marketing job in New York City two years ago, she moved to Houston and began freelancing as a content strategist.

“It made sense to base myself in a state that had no income tax, that had a lower cost of living,” said Cantú, 27.

Cantú and her boyfriend allocated $25,000 of their savings for a down payment and are currently shopping for a starter home they can build equity in and then sell.

Analisa Cantu, 27, is in the process of buying a house.

For someone like Bell, who is repairing her finances, homeownership will not be as immediate an option as it is for Cantú, but it isn’t out of reach.

“Have confidence in realizing that it won’t happen tomorrow,” said Lauren Bowling Seeger, Founder, Financial Best Life, a personal finance blog. Since interest rates will remain low for the next few years, there is no rush to jump into the housing market, she added.

Instead, use the next two to three years to chip away at debts at your own pace. Seeger recommends starting with small actions, such as cutting back on discretionary spending like subscription services, and, eventually, bigger swings like lowering your current housing costs.

“If you’re a renter, now is a good time to negotiate your rent with your landlord,” Seeger said.

Bell said she is optimistic that she will achieve her dream of being a property owner.

“I feel like it’s definitely still within my reach but when is questionable at this point,” she said. “I have friends who have done it. I’ve seen it and I know it’s not impossible.”