Robert Kueffer had always planned on going to graduate school but the global pandemic and economic uncertainty have fast-forwarded his plans.

Kueffer, who lost his job in February, moved back home to live with his parents in Wisconsin.

After months of searching, he was able to find a job and said that since he is living at home rent-free, he is now able to save about $3500 a month and is on track to save about half the cost of his MBA program.

“You realize how much money you spend like socializing, going out to eat, going to bars. When you stop doing that, you see the money just like pile up.”

The pandemic, while economically and emotionally devastating for millions of Americans, has also provided a unique opportunity to save and the time to explore potential career options. With low-interest rates and oftentimes lower tuition, now is the perfect time to go back to school.

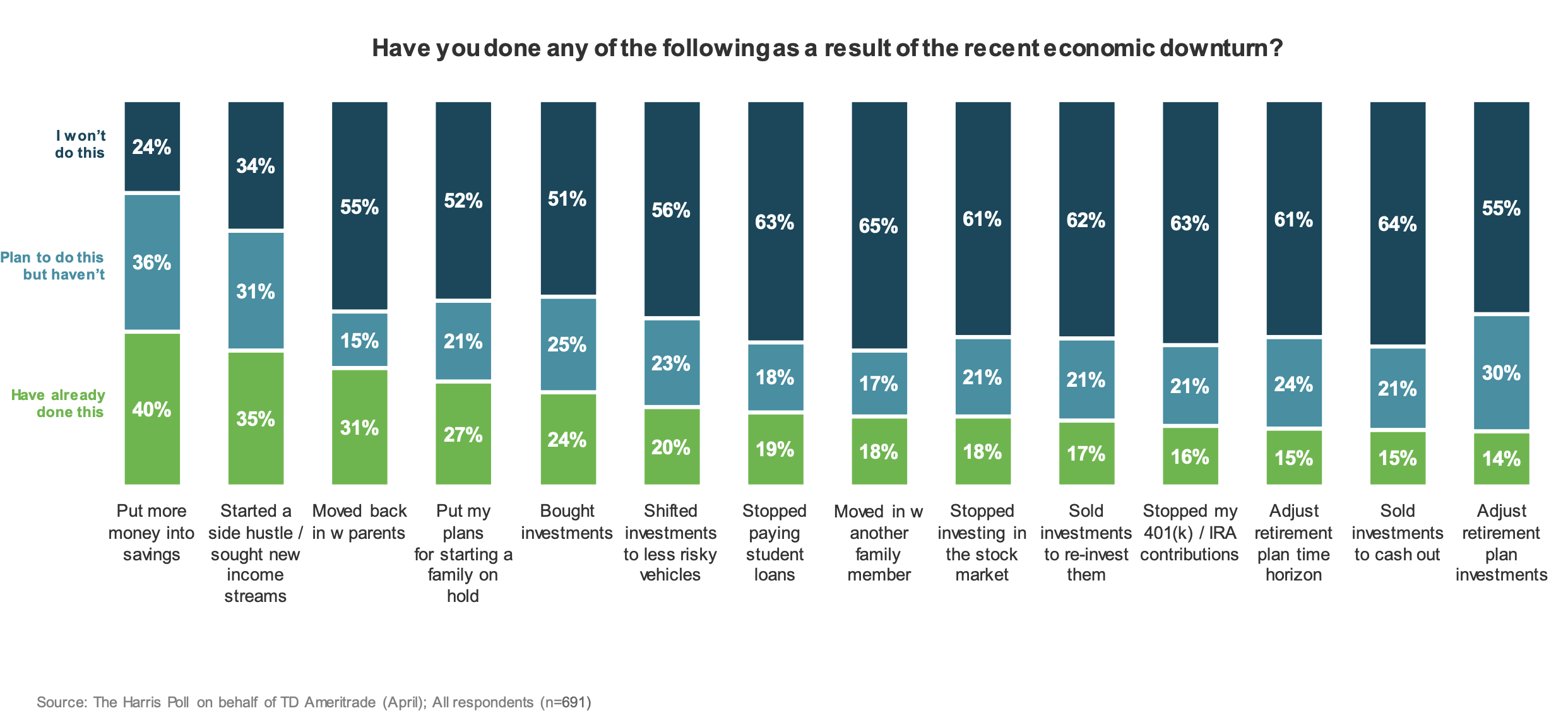

Like Kueffer, many younger millennials have moved back home with their families due to the pandemic and are now able to save more than they would have been able to otherwise.

An August survey conducted by TD Ameritrade found that 46% of the young adults surveyed had either moved back or were planning to move home with their parents and more than 76% had saved or were planning to save more due to the pandemic.

The federal student loan rate is also at a historical low, with undergraduate federal student loans set at a 2.75% interest rate, and graduate student loans set at a 4.3% interest rate.

Just last year, graduate federal direct unsubsidized loans had a 6.08% interest rate.

Federal student loans are fixed-term, meaning anyone taking out loans today, will have the same rate for the duration of that loan.

Additionally, the federal student loan rate, which is set by Congress every year on July 1, is based on the federal interest rate.

The Fed has indicated that they do not plan to raise rates until the end of 2023, so anyone contemplating going back to school right now will theoretically have the lowest rate on record for any loans taken out between now and June 30, 2024.

Many programs have also lowered tuition or offered additional need-based aid to students affected by the pandemic.

American University’s Kogod School of Business lowered their tuition rate by 10% this semester, said Jason Garner, director of Graduate Admissions at the Business school.

And this is something that schools may continue in the future.

Following the coronavirus shutdown, Johns Hopkins University School of Advanced International Studies (SAIS) created a COVID Relief Fund that offered need-based aid to students ranging from $1,000 to $8,000 for the semester, said Karen Ohen, director of Admission at SAIS.

The school, which mainly offers merit-based scholarship, is considering expanding its need-based aid model, to encompass incoming students for fall 2021, said Ohen.

“This year we’re hoping, it’s not official yet though, but we’re looking to still consider merit, but have some type of assessment on the need students may have moving forward. So I’m excited about what that could possibly pan out for the incoming class,” said Ohen.

There are downsides.

Potential students may have to contend with online classes for programs that are traditionally in-person and may have less opportunity to network.

However, the virtual environment, which many schools are considering turning into a permanent hybrid program, also provides an opportunity for some to attend schools in a location that may have previously been out of reach due to living costs or family situation.

Still, even with lower tuition, lower living costs, and additional savings, the cost of graduate schools can still run over a hundred thousand dollars for some programs.

Doyle, the financial counselor, said she tells students to only borrow up to the amount they can reasonably expect to earn in the first year of their career.

“What that means is that you’re investing the same amount that you’re going to earn,” said Doyle. “You know that you’ll be able to earn it back and it also will keep your debt payments affordable too.”

Student loans can also impair a person’s ability to get a mortgage down the line.

Mortgage lenders use something called the debt to income ratio when considering a mortgage application. This is the total amount of monthly debt, including student loan payments, someone owes divided by their gross monthly income.

“If that ratio is too high then it affects the amount of a mortgage you can get but it can also affect if you’re able to get a mortgage,” said Doyle.

“The biggest piece of advice for anybody who’s looking at returning to school is just do your research,” said Doyle.

Ultimately, the decision on whether to go back to school is up to each individual. But there is no doubt that lower interest rates, lower tuition, and the ability to save more at home have made going back to school cheaper and more accessible than it has ever been.